Food, Beverage & Agriculture – Industry Update Winter 2025

Key Themes across 2025

1. Health, Functional and Wellness Integration: Functional ingredients such as collagen, probiotics and adaptogens are now embedded in everyday food and drink, reflecting demand for preventative health. What was once a supplements category is now integrated into core FMCG.

In Q4, Supreme acquired the UK and European operations of SlimFast from Glanbia plc. Zydus Wellness also strengthened its position through the acquisition of Comfort Click, highlighting continued investor appetite for scalable, health-focused platforms.

2. Strategic Simplification Drives Deal Flow: Corporate portfolio rationalisation remained a defining feature, as large strategics continued to streamline operations and sharpen category focus. Groups divested non-core or slower-growth assets to concentrate capital on higher-margin, higher-growth segments such as health, premiumisation and branded platforms market.

3. Resilience and Pricing Power Shape Ingredients M&A: Trade buyers prioritised targets that improved margins, traceability and vertical integration, focusing on specialty ingredients and value-added processing to support pricing and protect supply in a volatile environment. Private equity remained active, backing scalable businesses with solid cash flow and operational upside. Notable transactions included Nexture’s acquisition of specialities manufacturer Oferta Genuina.

Engaging in future opportunities

Sentiment heading into 2026 remains optimistic, supported by a healthy pipeline of live processes and renewed sponsor engagement following improved financing conditions. With multiple assets already in market and corporates continuing to review portfolios, visibility on deal flow into H1 2026 is strong.

Over the Pond – 2025 Review and 2026 outlook

Deal Activity Begins to Accelerate

The last several months have seen a flurry of M&A activity in the food and beverage category, with both strategic and financial buyers showing a willingness to pay robust prices for high growth brands. Recent examples include Marzetti’s $400 million acquisition of Bachan’s, the breakout Japanese barbeque sauce brand; L Catterton’s majority investment in Good Culture, which valued the premium cottage brand at over $500 million and MPearlRock’s acquisition of The Good Crisp Co. Beyond brands, two of the largest publicly-traded private label platform announced they were being acquired – TreeHouse Foods by Investindustrial in a $2.9 billion transaction and SunOpta by Refesco in a $1.1 billion deal. Lastly, the IPO window appears to be cracking open as evidenced by Once Upon A Farm’s successful $198 million IPO, which valued the celebrity-backed baby food brand at nearly 4x revenue. In addition, Suja, a leading cold-pressed juice brand announced it has filed a registration statement and is expected to list shortly.

Food & Beverage Brands Still Dealing With Input Price Volatility

At the start of 2025, businesses and consumers were dealing with unprecedented spikes in egg and cocoa prices. While both of those commodities’ prices have returned to more normalized levels, coffee and beef prices have increased throughout 2025 and remain at extremely elevated levels. Companies have responded by selectively reformulating products, optimizing price pack architecture (a fancy way of saying “shrinkflation”) and as a last option, passing prices increases to an already stretched consumer.

Macroeconomic Indicators Sending Mixed Signals

In the U.S., economists and the markets are sorting through a mixed bag of economic statistics and trying to separate the message from the noise. On one hand, consumer sentiment remains depressed, fears of AI-driven job losses and elevated interest rates are constraining spending for consumers outside the top 10% income bracket, causing volume growth to be elusive for most businesses. On the other hand, the most recent jobs report came in stronger than expected, the most recent inflation reading was lower than expected and the stock market continues to set new highs.

2026 Outlook

Looking ahead to 2026, we remain optimistic. Our internal equity research indicates sustained strategic and financial buyer appetite, with valuation benchmarks trending ahead of prior expectations for high-quality assets. Demand is concentrated on differentiated brands, scaled manufacturing platforms and distribution businesses with defensible market positions. Overall, sector fundamentals remain supportive, underpinning a constructive outlook for the broader food & beverage market.

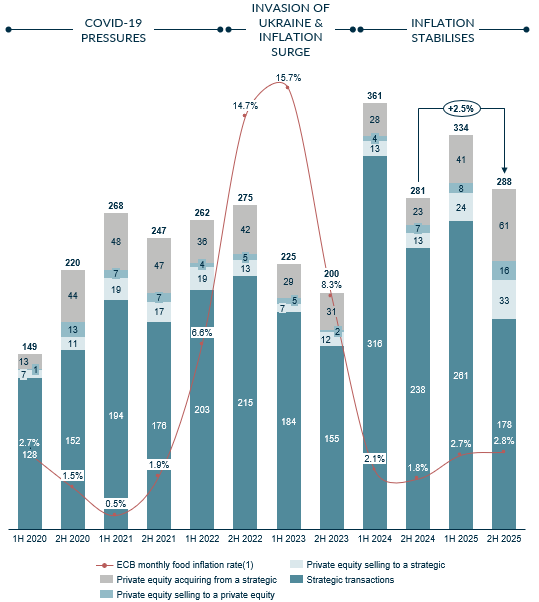

Snapshot of European Food, Beverage & Agriculture M&A deal activity

TAKING THE LONG VIEW – DEAL VOLUMES ARE STABILISING WITH 2H 2025 DEAL ACTIVITY SLIGHTLY EXCEEDING Y-O-Y

Number of announced acquisitions of European-based FB&A companies (deal value below USD 500m) & food inflation index rate from ECB

Note: 1) Rate calculated as the median rate Source: Mergermarket, European Central Bank

Download

The full report, including observations from ISM Cologne 2026, public company valuations & operating metrics as well as public comparables by subsector, can be downloaded at the top of the page.

Contact us

If you have any questions about the report, don’t hesitate to get in touch with one of our consumer team:

Ish Alg, Director

Andreas Kulcsar, Partner

Previous Food, Beverage & Agriculture Reports

Food, Beverage & Agriculture | M&A Industry Update | Q3 2025

Food, Beverage & Agriculture | M&A Industry Update | Q2 2025

Food, Beverage & Agriculture – M&A Industry Update – Q1 2025