Industrial Technology: Automation Market Update | Summer 2026

An Experienced, Proven, and Trusted Advisor in the Industrial Automation Sector

D.A. Davidson | MCF Finance Industrial Technology team is among the most experienced and active in the industry, with over 90 years of cumulative experience and over 200 global transactions completed. Our extensive experience and network of relationships worldwide allow us to provide a full range of highly customized M&A, debt advisory, and equity capital markets solutions to privately-owned, sponsored backed, and public companies around the world.

Industrial Technology Automation Update_Summer 2026_

Macroeconomic Update

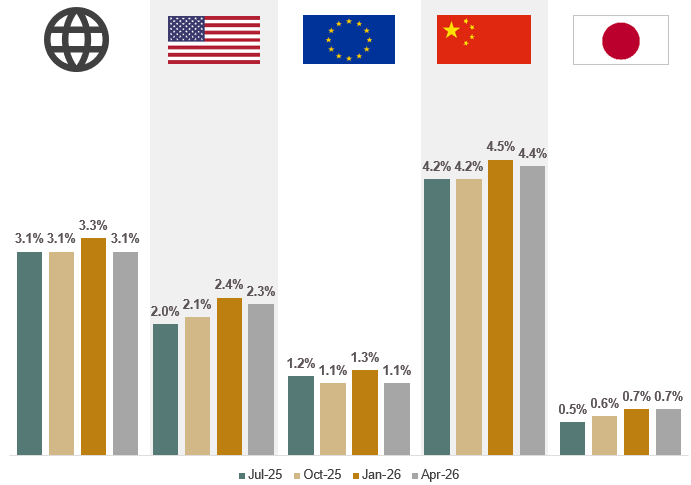

- Global real GDP growth for 2026 returned to 3.1% in April, with forecasts moderating as geopolitical tensions weigh on sentiment

- Economic conditions continue to be shaped by the scope and duration of conflict in the Middle East, and moderating trade tensions, highlighting areas to monitor within the broader outlook

- Potential upside remains meaningful, as productivity gains from AI adoption could support stronger economic growth over time, offering a constructive counterbalance to current headwinds

Real GDP Growth Forecast (2026)

Industrial & Manufacturing Performance Indicators

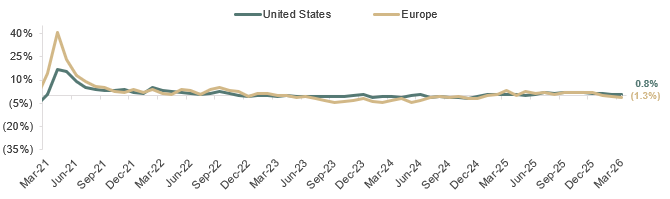

- U.S. industrial production has risen YoY for 15 consecutive months, reflecting steady improvement driven by easing supply chain constraints and steady demand; Europe saw a similar 12‑month expansion before softening in February and March 2026

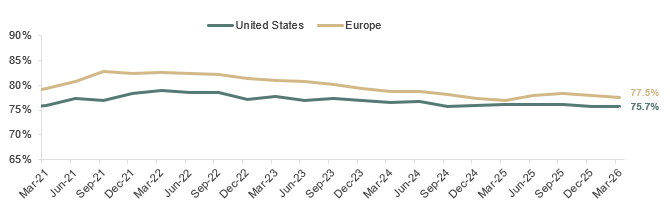

- Capacity utilization rates remained steady near 75%, with U.S. and European manufacturers operating at stable levels; disciplined capacity management and conservative capital spending have helped offset margin pressure from prior input cost increases

- Manufacturing sector conditions have largely stabilized following COVID-related disruptions in mid-2020 and the subsequent 2021 recovery; firms are maintaining a cautious but constructive outlook; while labor availability is still a challenge, customer ordering patterns show signs of strength and underlying demand trends continue to improve amid a gradually strengthening macro environment

Industrial Production Index (YoY Growth)

Capacity Utilization Index

Source: Federal Reserve Bank of St. Louis, European Commission Eurostat

Manufacturing Sentiment & Demand

- Manufacturing PMI readings in the U.S. rose to 54.0, the highest reading since May 2022, and Europe remained steady at 51.6, indicating a strengthening manufacturing economy in early 2026

- U.S. manufacturing new orders remained in expansion at 56.8 signaling that demand conditions continue to accelerate the pace of production

- Manufacturers are capitalizing on strengthening demand and accelerating production, though ongoing supply chain disruptions and geopolitical uncertainty continue to pressure input costs as the ISM Price Index registered 82.1 in May, near its highest level since 2022

Manufacturing Output & Backlog

- Manufacturing production remained strong throughout the start of 2026, with a reading of 54.3, indicating that output is rising to match the noticeable uptick in demand

- Manufacturing backlog has remained in expansion, driven by rising customer demand and tight labor conditions with the index reading 52.2 in May, a couple of months after recording a 56.6 mark in February that was the highest level since 2022

- Throughout 2025, output and backlog trends showed manufacturers carefully matching production to market demand; a sharp increase in production and backlog in the first half of 2026 underscores the importance of scalable operations as the predicted demand recovery in 2026 begins to materialize

Download

This edition features a thematic deep dive on Physical AI and its transformative impact on industrial and warehouse automation, including an innovation spotlight on AI-based safety and productivity solutions increasingly differentiated by software and controls. The report also provides commentary and key data trends across the factory automation, process automation, and warehouse automation sectors, and highlights metrics for key industry players and M&A deal activity.

The full report can be downloaded at the top of the page.

Contact us

If you have any questions about the report, don’t hesitate to get in touch with one of our team.

Dr Sven Harmsen, Partner

Franz Schranner, Partner